When applying for a car loan, lenders want to know how likely you are to repay the debt on time. While many consumers are familiar with traditional credit scores, auto lenders often rely on a specialized scoring model known as a FICO® Auto Score. This score is designed specifically to evaluate the risk associated with auto financing and can play a major role in determining whether you qualify for a loan, what interest rate you receive, and how much you can borrow.

One of the most commonly discussed versions is the fico auto score 8, a model that adjusts traditional credit scoring factors to better predict a borrower’s performance on vehicle loans. Understanding how this score works can help you make smarter financial decisions before shopping for a car.

Whether you’re purchasing your first vehicle, refinancing an existing auto loan, or simply preparing for a future purchase, learning about FICO Auto Scores can help you position yourself for better financing opportunities. This guide explains everything you need to know, including what a good score looks like, how to check your score, and practical strategies to improve it over time.

Quick Answer

A FICO® Auto Score is a specialized credit score used by vehicle lenders to assess the risk of lending money for a car purchase. Unlike general credit scores, it places greater emphasis on your history with auto loans and vehicle-related credit behavior.

The fico auto score 8 is one of several industry-specific scoring models developed by FICO. Auto lenders use these scores to estimate the likelihood that a borrower will make vehicle loan payments on time. Scores typically range from 250 to 900, with higher numbers indicating lower risk.

A strong FICO Auto Score can help you:

- Qualify for more loan options

- Secure lower interest rates

- Reduce monthly payments

- Increase approval odds

- Access better financing terms

Although lenders may use different versions of FICO Auto Scores, maintaining healthy credit habits generally benefits all scoring models.

What Is a FICO Auto Score?

A FICO Auto Score is a credit scoring model specifically created for the automotive lending industry. While traditional FICO Scores assess overall creditworthiness, Auto Scores focus on predicting the likelihood of default on vehicle financing.

The scoring model analyzes information from your credit report, including payment history, outstanding debt, credit utilization, account age, and previous loan performance. However, it gives additional weight to behaviors that are especially relevant to auto lending.

For example, if you successfully managed previous car loans and consistently made payments on time, that positive history may have a stronger impact on your Auto Score than on your general credit score.

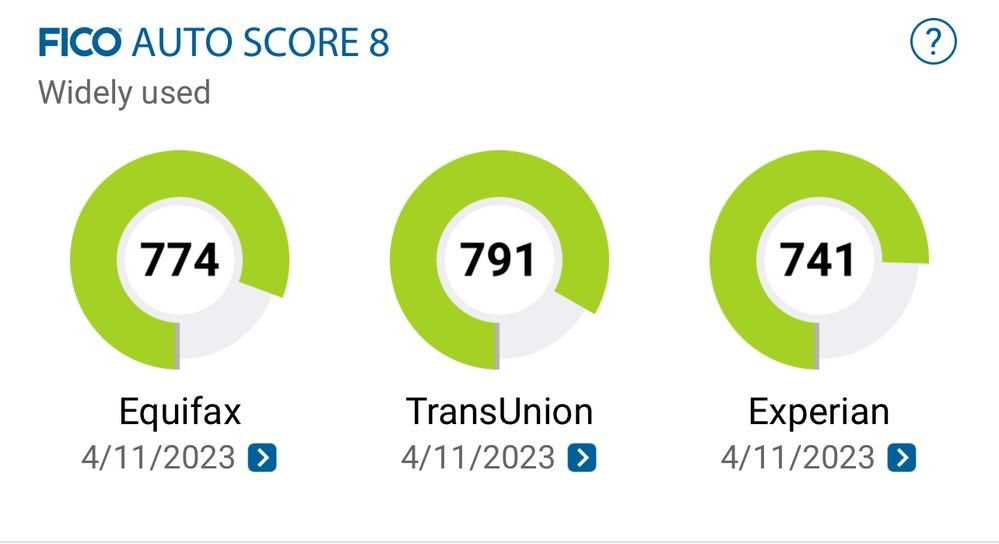

There are several versions of FICO Auto Scores, including Auto Score 2, Auto Score 4, Auto Score 5, Auto Score 8, Auto Score 9, and Auto Score 10. Different lenders may use different versions depending on their lending criteria and the credit bureau providing the data.

The fico auto score 8 remains one of the most recognized models because it balances modern credit assessment techniques with broad industry adoption.

Get your FICO® ScoreΘ for free

Many consumers assume they must pay to access credit scores, but there are several ways to obtain a free FICO Score. While free services may not always provide every version of the Auto Score, they can offer valuable insight into your overall credit health.

A free credit score can help you understand where you stand before applying for a vehicle loan. Monitoring your score regularly also allows you to identify potential problems early and take corrective action.

No credit card required

Many financial institutions, credit card issuers, and credit monitoring services offer free access to credit scores without requiring payment information. This allows consumers to track their credit standing without committing to a subscription.

These services often provide monthly updates and educational resources that explain changes in your credit profile.

No impact to your FICO® Score

Checking your own credit score is considered a soft inquiry. Unlike a hard inquiry initiated by a lender during a loan application, a soft inquiry does not affect your credit score.

You can review your score as often as needed without worrying about harming your creditworthiness.

Understand your FICO® Score

Beyond simply displaying a number, many score providers explain the factors influencing your score. This information can help you identify strengths and weaknesses in your credit profile.

Understanding what affects your score allows you to make informed decisions that support long-term financial health and stronger borrowing opportunities.

What Is a Good FICO Auto Score?

A good FICO Auto Score varies somewhat between lenders, but higher scores generally lead to better financing options. Auto lenders use score ranges to categorize borrowers according to risk.

The following table provides a general overview:

| FICO Auto Score Range | Credit Quality | Typical Lending Impact |

| 800–900 | Exceptional | Best rates and terms |

| 740–799 | Very Good | Highly favorable financing |

| 670–739 | Good | Competitive loan offers |

| 580–669 | Fair | Higher rates possible |

| 250–579 | Poor | Limited financing options |

Borrowers with scores above 740 often qualify for the lowest interest rates available. This can result in significant savings over the life of an auto loan.

For example, two borrowers purchasing identical vehicles may receive dramatically different interest rates based solely on their credit profiles. Even a small difference in interest rate can translate into thousands of dollars in total loan costs.

It’s also important to understand that lenders evaluate more than just your score. Income, employment history, debt-to-income ratio, down payment amount, and loan term all influence lending decisions.

Even if your score falls below the ideal range, improving it before applying can substantially increase your borrowing power and reduce overall financing costs.

Read Also: https://dailyvival.com/aeonscope-net/

How to Check Your FICO Auto Score

Checking your FICO Auto Score can help you understand how lenders may view your credit application before you begin shopping for a vehicle.

Unlike standard credit scores, Auto Scores are not always available through free services. Some premium credit monitoring subscriptions provide access to multiple versions of industry-specific FICO Scores, including Auto Scores.

When reviewing your score, remember that lenders may use different versions depending on their internal policies and preferred credit bureau. As a result, the score you see may not exactly match the one used during your application.

Even so, monitoring your score remains valuable because most FICO scoring models move in similar directions. If your general FICO Score improves, your Auto Score will often improve as well.

Before checking your score, gather information from all three major credit bureaus. Reviewing your credit reports allows you to identify inaccuracies, fraudulent activity, or outdated information that could affect your score.

Regular monitoring is particularly useful if you plan to purchase a vehicle within the next six to twelve months. It gives you time to correct issues and improve your credit profile before lenders evaluate your application.

How to Improve Your FICO Auto Score

Improving your FICO Auto Score requires consistent credit management rather than quick fixes. The good news is that many of the same habits that strengthen traditional credit scores also support better auto lending scores.

Payment history remains the single most influential factor. Making every payment on time demonstrates reliability and significantly improves your credit profile. Even one late payment can remain on your credit report for years and negatively impact future lending decisions.

Credit utilization is another major component. High balances relative to available credit limits can signal financial stress. Paying down revolving debt often produces noticeable score improvements.

Length of credit history also matters. Older accounts provide evidence of long-term credit management. Closing established accounts unnecessarily may reduce your average account age and lower your score.

Limiting new credit applications is equally important. Multiple hard inquiries within a short period can indicate elevated borrowing risk. While rate-shopping for an auto loan is generally treated differently by scoring models, excessive applications for other forms of credit may still affect your profile.

Diversifying your credit mix can also contribute positively. Consumers who responsibly manage multiple account types, such as credit cards, installment loans, and mortgages, often demonstrate stronger credit management skills.

Finally, review your credit reports regularly. Errors such as incorrect balances, duplicate accounts, or fraudulent activity can artificially depress your score. Correcting inaccuracies can lead to meaningful improvements without changing your financial behavior.

Building a strong FICO Auto Score takes time, but consistent responsible credit habits produce lasting results that extend beyond auto financing.

The Bottom Line

A FICO Auto Score provides lenders with a specialized assessment of your ability to manage vehicle-related debt. While there are multiple versions available, the fico auto score 8 remains one of the most recognized and widely discussed models in auto lending.

Understanding how Auto Scores differ from traditional credit scores can help you prepare more effectively before applying for a vehicle loan. Factors such as payment history, credit utilization, account age, and previous auto loan performance all contribute to your score.

The higher your score, the greater your chances of securing favorable financing terms, lower interest rates, and reduced borrowing costs. Even small improvements can result in significant savings throughout the life of a loan.

Monitoring your credit, correcting report errors, reducing debt, and maintaining consistent payment habits are among the most effective ways to strengthen your score over time. By taking proactive steps today, you can improve your financial position and gain access to better vehicle financing opportunities in the future.

What makes a good FICO Auto Score 8?

A good FICO Score reflects responsible credit management and demonstrates to lenders that you are a reliable borrower. While exact standards vary, scores of 670 and above are generally considered good across most lending categories.

A strong FICO Score is built through several key behaviors. Consistently paying bills on time establishes a positive payment history. Keeping credit card balances low relative to available limits shows responsible use of revolving credit. Maintaining older accounts helps strengthen credit history, while avoiding excessive applications reduces unnecessary inquiries.

Lenders often view borrowers with higher scores as less risky, which can lead to lower interest rates, better loan terms, and greater approval odds. This applies not only to auto loans but also to mortgages, personal loans, and credit cards.

It’s important to remember that credit scores are dynamic. They change as new information appears on your credit report. Small improvements made consistently over time can produce meaningful long-term results.

Ultimately, a good FICO Score is not just about achieving a specific number. It represents healthy financial habits that support borrowing flexibility, lower costs, and greater financial opportunities throughout life.

Frequently Asked Questions

1. Is FICO Auto Score different from a regular credit score?

Yes. A FICO Auto Score is specifically designed for vehicle lending and places greater emphasis on factors related to auto loan repayment behavior.

2. What is the highest possible FICO Auto Score?

Most FICO Auto Score models range from 250 to 900, with 900 being the highest achievable score.

3. Can I get a car loan with a low FICO Auto Score?

Yes, but you may face higher interest rates, larger down payment requirements, or fewer financing options compared to borrowers with stronger scores.

4. How often does a FICO Auto Score update?

Your score can update whenever new information is reported to the credit bureaus, typically monthly as lenders submit account activity.

5. Does paying off a car loan improve my FICO Auto Score?

Successfully paying off an auto loan can strengthen your credit history and demonstrate responsible borrowing behavior, which may positively influence future Auto Scores.

Conclusion

The fico auto score 8 is an important tool used by auto lenders to evaluate borrowing risk and determine loan eligibility. Unlike general credit scores, it focuses specifically on factors that predict vehicle loan repayment performance. Understanding how the score works gives consumers a valuable advantage when preparing for a car purchase.

By maintaining on-time payments, reducing debt, monitoring credit reports, and practicing responsible credit management, borrowers can improve their scores and qualify for better financing opportunities. Whether you’re buying your first vehicle or refinancing an existing loan, a strong FICO Auto Score can translate into lower interest rates, reduced monthly payments, and significant long-term savings.